It’s been a while since I last talked about @maplefinance.

Since then, the business has continued to grow while the token has stalled.

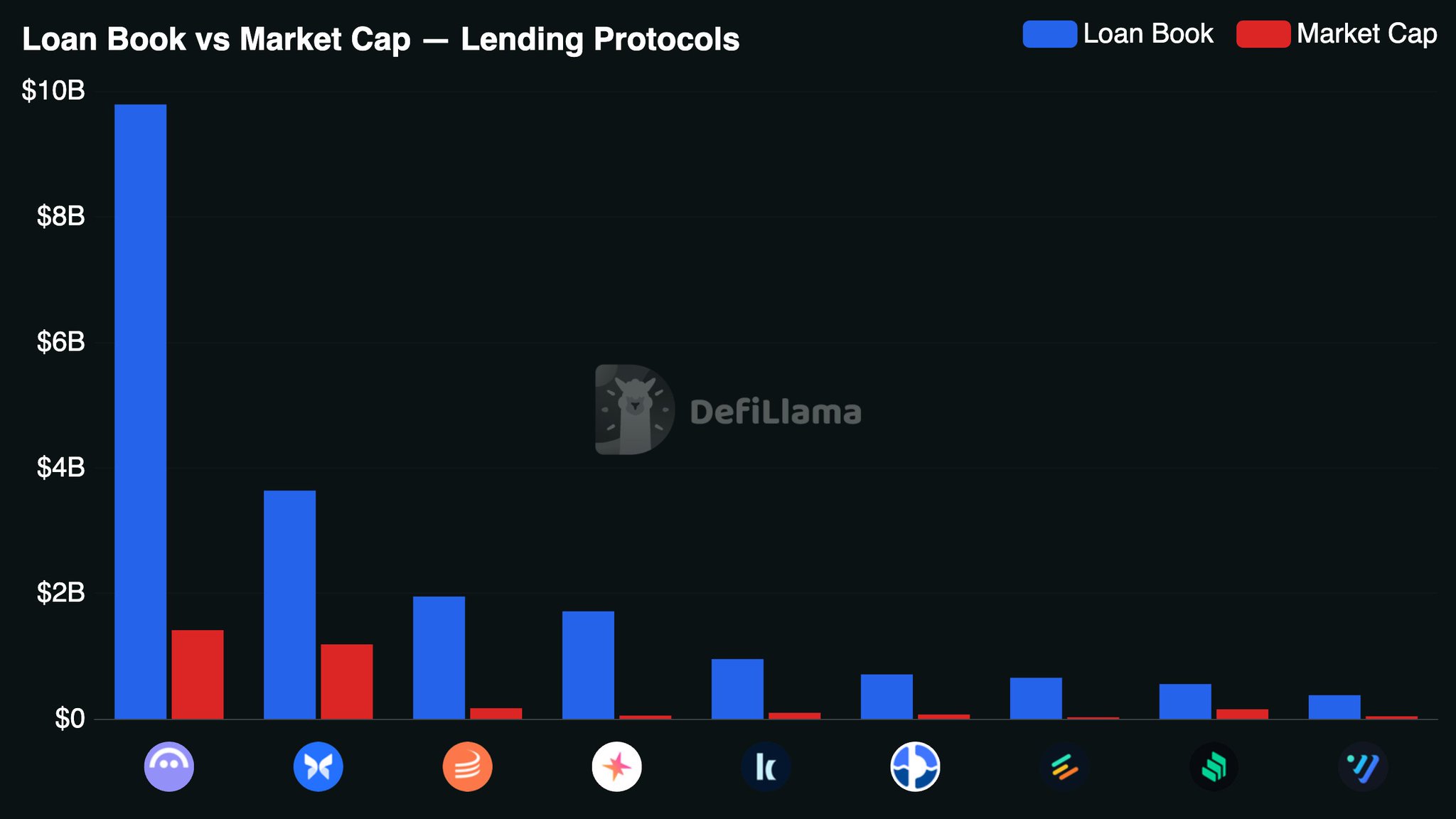

$1.93B loan book to the $SYRUP token at $162M, -78% for the year.

The market has clearly written them off. A similar event happened in 2022 when the Maple team was written off.

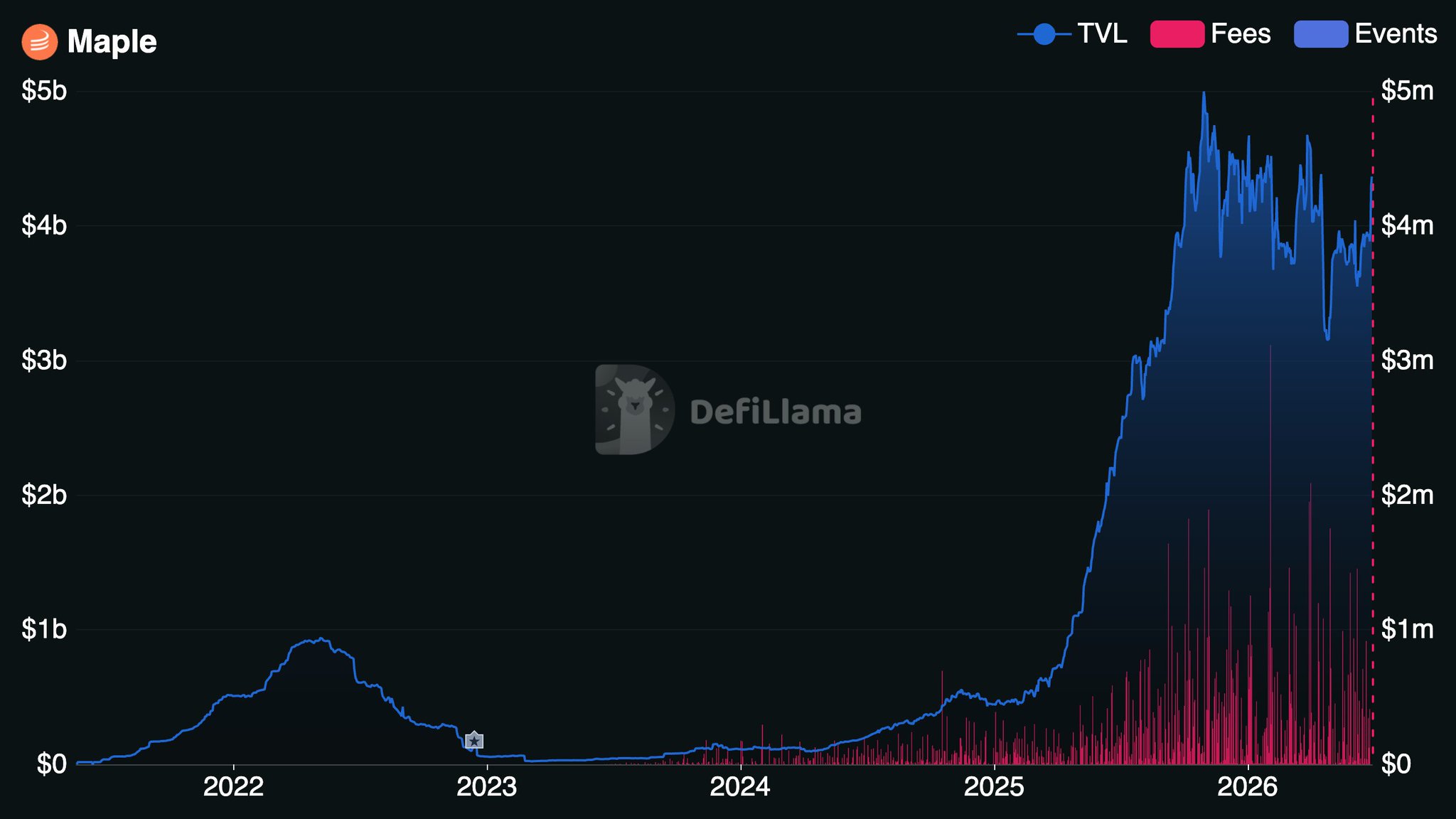

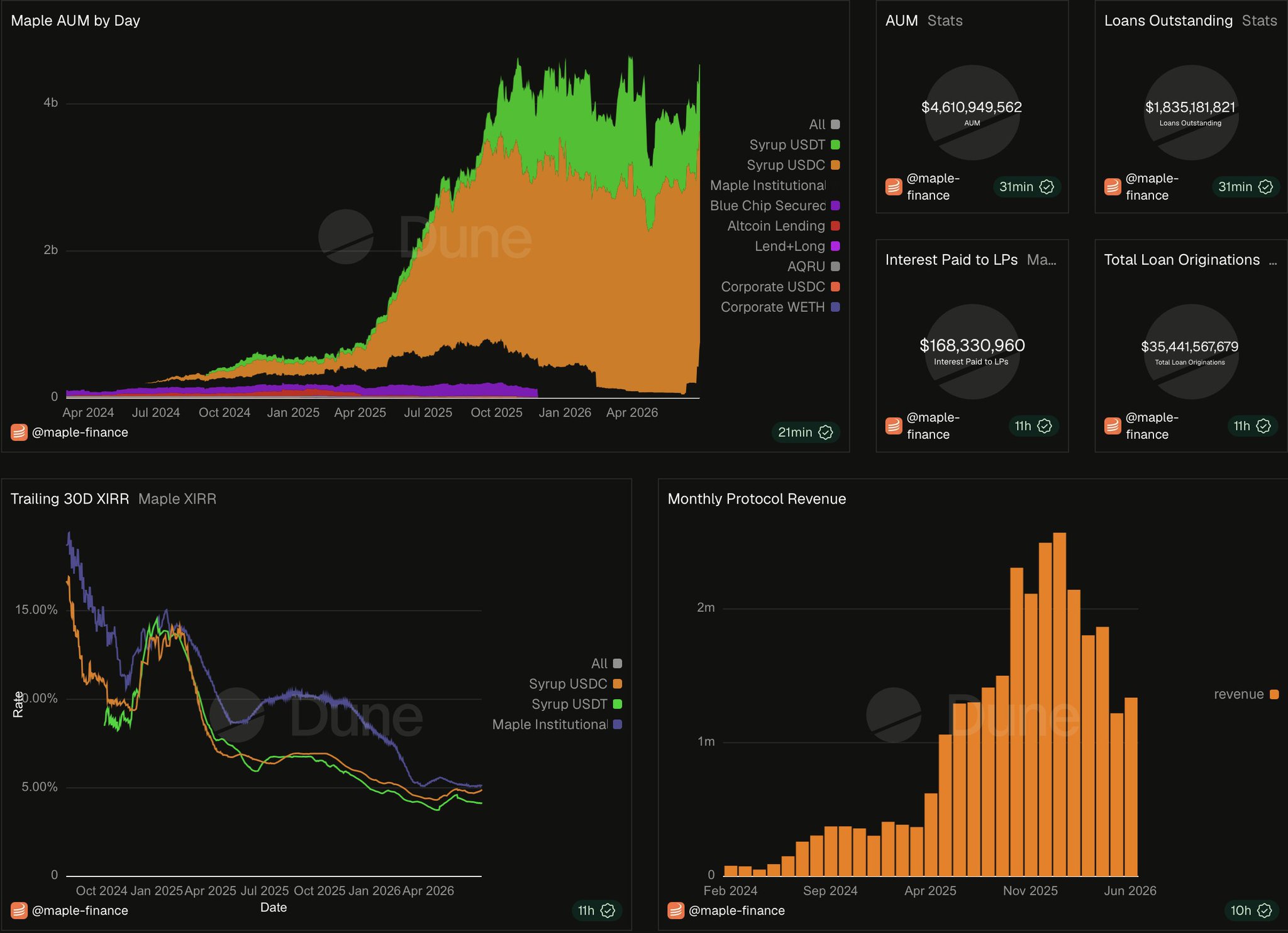

Fast forward to today with a new model, and the loan book looks significantly healthier at $1.93B, with 82.9% utilization.

Maple also generates $12.8M in annualized protocol revenue through management and service fees, separate from the interest flowing to lenders.

25% of that revenue is allocated to return to $SYRUP via discretionary buybacks.

That's $2.86M annualized against a $162M market cap, and the mechanism has been live since November.

Now compare that to the lending peer set:

$MORPHO trades at a $1.17B market cap with $0 in protocol revenue.

(Morpho trades at 7.2x Maple’s mktcap)

$KMNO at $97M and $FLUID at $68M both trade near Maple on P/S, at 13.7x and 15.3x respectively, but neither has an active buyback mechanism.

$SYRUP is trading at 14.2x P/S with:

- A $1.93B loan book

- 82.9% utilization

- Discretionary SYRUP buybacks

- @krakenfx OTC as a new borrower pipeline

- syrupUSDT now used as collateral inside one of DeFi’s deepest lending markets

The fundamentals really make the valuation harder to ignore down here.

The main point here is that Maple is running a $1.93B credit book while the market is still pricing it like its 2022 version.