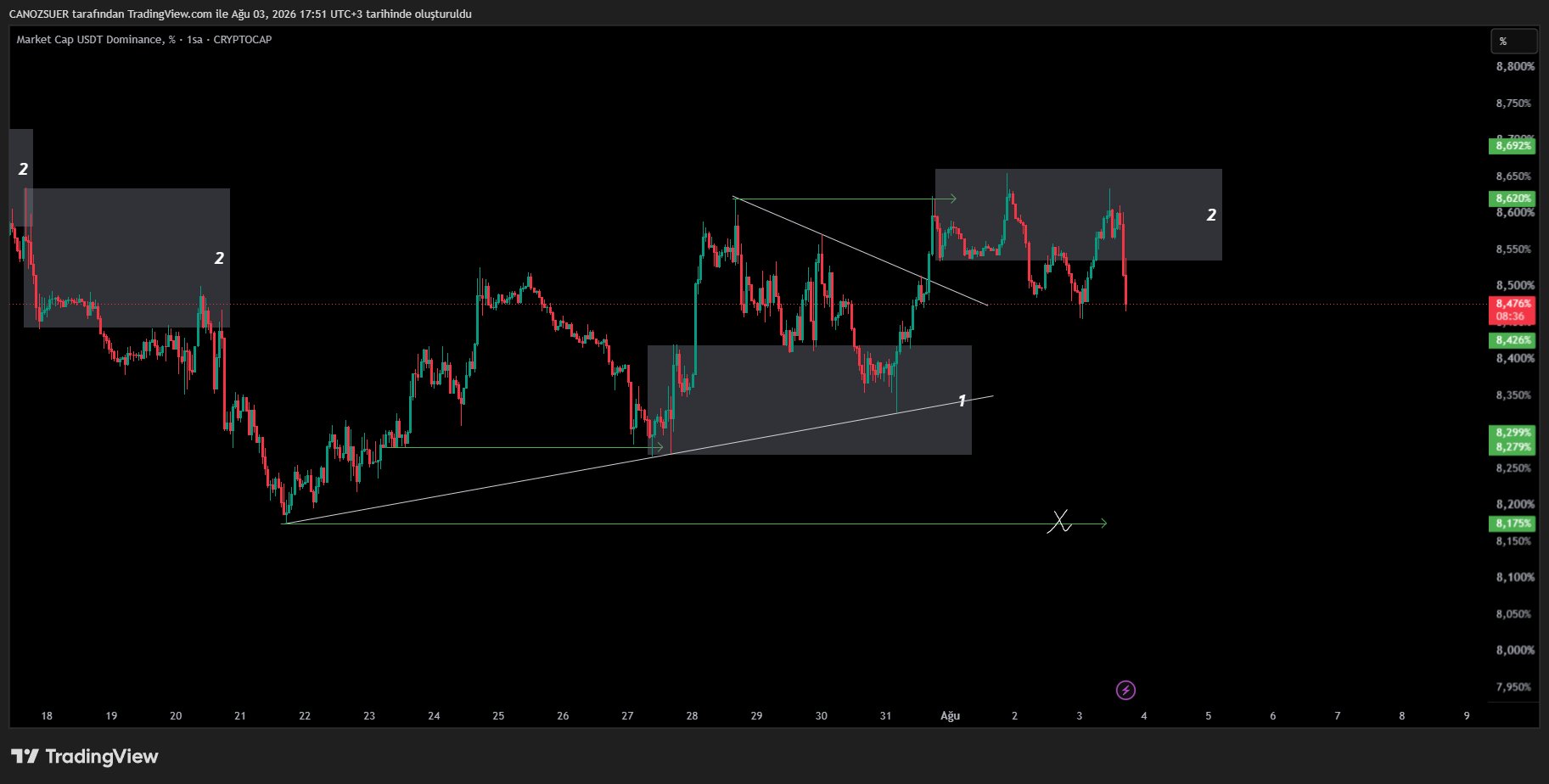

We've discussed this setup multiple times already, don't force trades within the marked zone. Chasing price in a volatile range is one of the fastest ways to lose money. Once again, I'm reminding you to protect your capital and stay patient.

The real opportunity will come after a confirmed breakout or breakdown. Until then, it's better to stay out of the market and wait for high-probability setups.

DYOR, NFA

#USDTD #TETHER