Been tagged a couple of times on this post and have received a few DMs about it.

My position hasn't changed. I'm still heavily invested in $VELO @veloprotocol

There's honestly not much more to say. We follow the progress, the milestones, the partnerships, and the execution. I'm a spot-and-hold investor. My portfolio is already positioned.

I believe in macro cycles, liquidity, and high-timeframe market structure. I also believe those who understand where this industry is heading are quietly positioning themselves accordingly.

Some projects build loudly and keep the timeline entertained every day. Others stay in stealth mode, execute quietly, and let the fundamentals speak over time. Choose the thesis that makes sense to you, then invest accordingly.

As for me, I'm still 100% committed to $VELO.

I've just been spending less time on here because I'm busy with projects outside this platform.

To be honest, X has become a bit oversaturated for me, and I was starting to feel like a broken record repeating the same things.

That said, there are some great accounts on here and some genuinely great people I've connected with, and I'll still jump in from time to time.

But there's really nothing more to say. You can either spend your days on here waiting for the cycle to play out, or you can be more productive offline, get on with life, and let the bloody cycle do its thing.

Leaving Thailand for a few months and heading back to Sydney next month for a change of scenery. Hopefully I'll be celebrating the run over there. 💥

I'm not going anywhere. See you all at the end of the cycle and sometimes in between. 🍻

Velodrome Finance 實時價格數據

Velodrome Finance VELO 價格歷史 USD

Velodrome Finance 社交媒體動態

2.0K @shanesek1

2.0K @shanesek1  152.6K @CrytexIntel

152.6K @CrytexIntel 🔎 VELO — Velo Protocol — CRYPTEX INTEL

Current price: ~$0.0034 | Market cap: ~$60M

VELO is the coordination token for a PayFi network targeting the exact problem SWIFT was built to solve — and doing it without a correspondent banking chain.

The protocol pivoted hard in May 2026 with a new whitepaper and PAYFAI system — an AI-driven settlement layer for global FX liquidity and treasury management. That's not a minor update. It's a full architectural shift from cross-border payments protocol to crypto-native FX treasury network for compliant global settlement.

What's building in 2026:

🔹 Orbit Plus consumer SuperApp live across 15 countries — virtual crypto debit card, Apple/Google Pay compatible, direct crypto-to-bank off-ramp

🔹 Q3 2026: RWA tokenization + cross-chain swaps + first whitelabel partner launch

🔹 Q4 2026–2027: Treasury-as-a-Service commercial rollout, VELO staking for LPs, support for 100+ business tenants

🔹 USD1 stablecoin integration (World Liberty Financial) — institutional-grade stablecoin

72

72

5

5

3.0K

3.0K

3.0K @MarcoSalzmann80

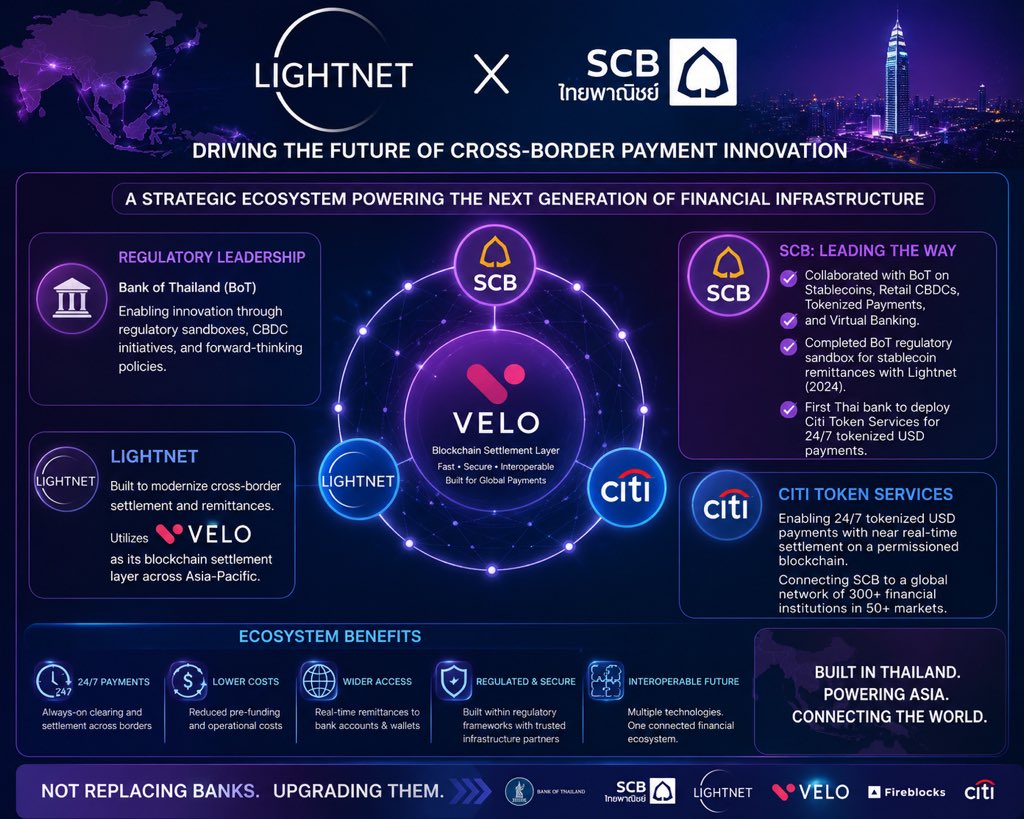

3.0K @MarcoSalzmann80 🧵 SCB just became the first Thai bank to use Citi Token Services for 24/7 tokenized USD payments. 🇹🇭

But this raises a bigger question…

Why is Thailand becoming one of the world’s most advanced blockchain banking markets?

The answer isn’t just Citi.

It’s an entire financial ecosystem.

👇

For years, the Bank of Thailand has taken a very different approach from many Western regulators.

Instead of resisting blockchain…

It created regulatory sandboxes.

Banks were encouraged to test new financial infrastructure under regulatory supervision before launching it commercially.

That changed everything.

One of the biggest examples?

@scb_thailand

Thailand’s oldest commercial bank.

SCB didn’t simply experiment with blockchain.

It worked directly with the Bank of Thailand on:

• Stablecoins

• Retail CBDCs

• Tokenized payments

• Virtual banking

Each project moved from controlled testing into real-world deployment.

One milestone came in 2024.

SCB and @lightnetgroup completed the Bank of Thailand’s regulatory sandbox for blockchain-based stablecoin remittances.

The service was approved for commercial deployment using Fireblocks for digital asset custody.

That wasn’t speculation.

It was regulated financial infrastructure.

Lightnet itself wasn’t built as a consumer crypto platform.

It was designed to modernize cross-border settlement.

Lightnet utilizes the Velo Protocol as its blockchain settlement layer for cross-border payments across Asia-Pacific.

Now comes the latest announcement.

@scb_thailand has become the first bank in Thailand to deploy Citi Token Services for 24/7 tokenized USD payments.

Different technology.

Different platform.

Same direction.

Notice the pattern?

The Bank of Thailand.

@scb_thailand

@lightnetgroup

@veloprotocol

@FireblocksHQ

@Citi

They’re not building one single product.

They’re modernizing different layers of the same financial system.

Some focus on tokenized deposits.

Others on stablecoins.

Others on blockchain settlement.

Others on regulated banking.

Each solves a different piece of the puzzle.

That’s why @veloprotocol remains relevant.

Not because Citi suddenly uses Velo.

But because the same market that embraced regulated stablecoin settlement through Lightnet is now embracing tokenized institutional payments through Citi.

Both developments point toward programmable financial infrastructure.

The question is no longer:

“Will banks adopt blockchain?”

Thailand already answered that.

The real question is:

How will tokenized deposits, stablecoins and blockchain settlement eventually work together?

Thailand may be one of the first countries showing what programmable financial infrastructure actually looks like.

Not replacing banks.

Upgrading them.

820 @CristianIonita6

820 @CristianIonita6 Thailand’s SCB keeps leading on tokenized payments!

Just announced: SCB is the first Thai bank (and first globally) to go live with @Citi’s 24/7 USD Clearing + Citi Token Services on a private permissioned blockchain for real-time cross-border USD payments.

This builds on SCB’s earlier moves in the space — including its longstanding partnership with @lightnetgroup, which powers remittances using the @veloprotocol blockchain for efficient, compliant cross-border settlements.

SCB is clearly positioning itself at the forefront of tokenized finance in Southeast Asia. From private chains to public protocol integrations — the rails are getting built. 🌏

#Tokenization #CrossBorderPayments #Blockchain #Fintech #Thailand #PayFi https://t.co/gu2fIicq44

91

5

5.3K

3.0K @MarcoSalzmann80 🧵 SCB just became the first Thai bank to use Citi Token Services for 24/7 tokenized USD payments. 🇹🇭

But this raises a bigger question…

Why is Thailand becoming one of the world’s most advanced blockchain banking markets?

The answer isn’t just Citi.

It’s an entire financial ecosystem.

👇

For years, the Bank of Thailand has taken a very different approach from many Western regulators.

Instead of resisting blockchain…

It created regulatory sandboxes.

Banks were encouraged to test new financial infrastructure under regulatory supervision before launching it commercially.

That changed everything.

One of the biggest examples?

@scb_thailand

Thailand’s oldest commercial bank.

SCB didn’t simply experiment with blockchain.

It worked directly with the Bank of Thailand on:

• Stablecoins

• Retail CBDCs

• Tokenized payments

• Virtual banking

Each project moved from controlled testing into real‑world deployment.

One milestone came in 2024.

SCB and @lightnetgroup completed the Bank of Thailand’s regulatory sandbox for blockchain‑based stablecoin remittances.

The service was approved for commercial deployment using Fireblocks for digital asset custody.

That wasn’t speculation.

It was regulated financial infrastructure.

Lightnet itself wasn’t built as a consumer crypto platform.

It was designed to modernize cross‑border settlement.

Lightnet utilizes the Velo Protocol as its blockchain settlement layer for cross‑border payments across Asia‑Pacific.

Now comes the latest announcement.

@scb_thailand has become the first bank in Thailand to deploy Citi Token Services for 24/7 tokenized USD payments.

Different technology.

Different platform.

Same direction.

Notice the pattern?

The Bank of Thailand.

@scb_thailand

@lightnetgroup

@veloprotocol

@FireblocksHQ

@Citi

They’re not building one single product.

They’re modern izing different layers of the same financial system.

Some focus on tokenized deposits.

Others on stablecoins.

Others on blockchain settlement.

Others on regulated banking.

Each solves a different piece of the puzzle.

That’s why @veloprotocol remains relevant.

Not because Citi suddenly uses Velo.

There is no public evidence of that.

But because the same market that embraced regulated stablecoin settlement through Lightnet is now embracing tokenized institutional payments through Citi.

Both developments point toward programmable financial infrastructure.

The question is no longer:

“Will banks adopt blockchain?”

Thailand already answered that.

The real question is:

How will tokenized deposits, stablecoins and blockchain settlement eventually work together?

Thailand may be one of the first countries showing what programmable financial infrastructure actually looks like.

Not replacing banks.

Upgrading them.

820 @CristianIonita6

820 @CristianIonita6 Thailand’s SCB keeps leading on tokenized payments!

Just announced: SCB is the first Thai bank (and first globally) to go live with @Citi’s 24/7 USD Clearing + Citi Token Services on a private permissioned blockchain for real-time cross-border USD payments.

This builds on SCB’s earlier moves in the space — including its longstanding partnership with @lightnetgroup, which powers remittances using the @veloprotocol blockchain for efficient, compliant cross-border settlements.

SCB is clearly positioning itself at the forefront of tokenized finance in Southeast Asia. From private chains to public protocol integrations — the rails are getting built. 🌏

#Tokenization #CrossBorderPayments #Blockchain #Fintech #Thailand #PayFi https://t.co/gu2fIicq44

0

0

37

價格預測

什麼時候是購買VELO的好時機?我應該現在買入還是賣出VELO?

Beacon預測

概率價格預測(未來24小時)此預測為實驗性技術產品,僅供參考,不構成投資建議。現實生活中的任何突發事件都可能對交易行為產生重大影響,因此交易者應謹慎決策。